Halaman yang Anda Cari Tidak Tersedia

Halaman yang Anda Cari Tidak Tersedia

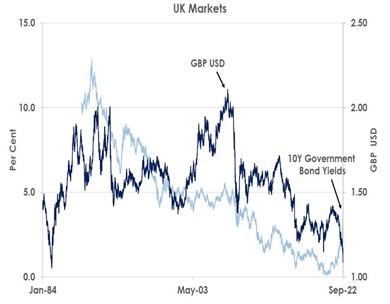

The GBP and UK bond yields have become highly volatile since Britain’s new government unveiled sweeping unfunded tax cuts last month, raising serious risks to the economic outlook.

The GBP fell to record lows of 1.0350 against the USD as the chart shows while government bond yields soared from 3.30% to 4.50% for 10Y gilts.

Financial markets plunged because the government’s tax cuts would sharply weaken Britain’s already precarious economic position.

The UK is set to enter recession as the energy shock from the war in Ukraine squeezes consumption while, at the same time, raising inflation in Britain to double digits. In response, the government announced earlier last month it would freeze energy bills to support households and firms at an estimated cost of GBP60 billion for the next six months.

The mini-budget’s tax cuts would result in another GBP45 billion of lost revenues, raising the government’s fiscal deficit to over 7% of GDP. With the UK running a huge current account deficit over 8% of GDP, the shocking fiscal news made global investors wary at funding the UK’s ‘twin deficits’, causing the GBP to dive and gilt yields to soar. This forced the Bank of England to undertake emergency action to protect UK pension funds by buying government bonds last week and the BoE pledged it would continue to intervene in the gilts market until October 14.

Source: Bank of Singapore, Bloomberg.

Faced with a disastrous response to its mini-budget, the government has begun to backtrack, announcing it would keep the highest rate of income tax at 45%. Its concession has helped the GBP recover to its pre-mini budget levels around 1.13 against the USD. However, the economic and political crisis is far from over.

Firstly, keeping the 45% income tax rate will only save GBP2-3 billion compared to the GBP45 billion of revenues the government would lose from all the tax cuts in its mini-budget. Either the government will have to give up more of its proposed tax cuts or make politically difficult spending cuts when the UK is entering recession. The UK Chancellor says he will set out more detailed fiscal plans before the end of the month. However, the Office for Budget Responsibility’s independent forecasts may not be supportive.

Secondly, the BoE may keep intervening to stop bond yields rising this month but at its November 3 meeting it will need to raise interest rates sharply to offset the inflation caused by GBP weakness and greater government borrowing. We now expect a 100bps hike next month and 50bps rises in December and February, lifting the Bank Rate from 2.25% to 4.25% by early 2023.

Lastly, the severe blow to UK credibility will make investors cautious of funding Britain’s fiscal and current account deficits. We thus think it is likely the GBP will fall back towards its new record lows against the USD over the next few months.

This article was first published by Bank of Singapore on October 4, 2022. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Bank OCBC NISP Private Banking Tbk. or its affiliates.

OCBC NISP Private Banking provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC NISP Private Banking is a part of OCBC Group.