Halaman yang Anda Cari Tidak Tersedia

Halaman yang Anda Cari Tidak Tersedia

Concerns over the second waves of infections impacted investor behavior

Not for the first time this month, the sharp equity rally that began in late March saw its momentum stall late last week as concerns over second waves of infections affected investor sentiment.

We see the risk of rising Covid-19 infections in US states such as Florida, Texas and Arizona to be a wildcard for markets, and there is still limited clarity. It is of note that the overall death rate in the US appears to paint a less worrying picture versus the infection rate at this point. For the whole of the US excluding New York, while the 7-day average infection rate has risen by about 50% over the month to date, the rate of new deaths has in fact declined by approximately 30%. In addition, the rise in infection seems to be more skewed towards younger people, for whom the virus is less likely to be fatal and therefore are more likely to return to pre-Covid-19 behavior.

Notwithstanding an ongoing debate over whether the rise in infections is in fact a second wave or is simply the later leg of the first wave, the key implication is that a persistent rise in Covid-19 cases would form a major impediment to easing of containment measures and the momentum of the economic recovery.

Adding to the list of risks for the market trajectory was also uncertainty related to the US Presidential Elections as President Trump’s polling numbers continue to slide amidst nationwide protests.

Our view is that a Biden win with a Republican Senate and Democrat House would likely be the best scenario for markets over the long term, as we would see a more measured approach from the White House towards the US-China relationship while Trump’s tax cuts are unlikely to be rolled back with a Republican Senate.

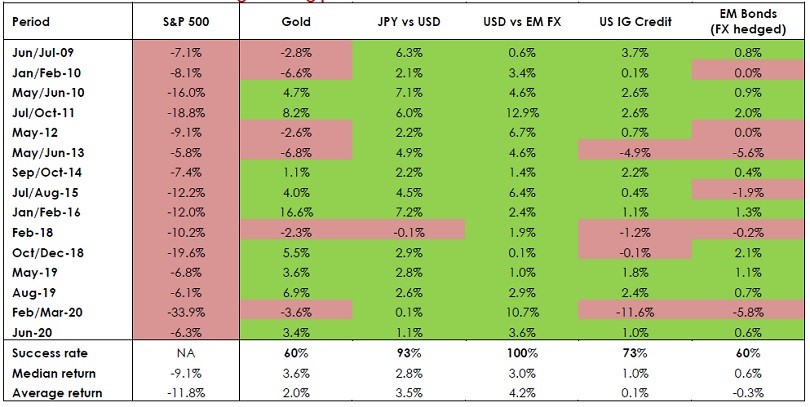

Exhibit 1: Return on various hedges during periods of S&P500 drawdowns since 2009

Source: Bloomberg, Bank of Singapore, JP Morgan; as at 26 June 2020 Note: Chart shows returns on hedges during largest S&P500 drawdowns since 2009. S&P500 drawdown calculated as maximum peak-to-trough move during period. Returns on other asset classes defined as total return over that same period. Green shading indicates positive return on hedge during equity decline. EM = Emerging Market. IG = Investment Grade. The information presented is historical information and past performance is not a guarantee or indication of future results

Following this, the second-best outcome for markets would be a Trump win.

Finally, a Democrat sweep of the White House and Congress would be the outcome most detrimental to markets given the likelihood of higher corporate and capital gains taxes. Already, betting markets and polls at key states for the US Presidential elections and at-risk Republican Senate seats are reflecting a rising probability of a scenario of a Democrat sweep.

As for now, this is still some distance away: historically, the US election comes into focus as a market driver in the second half of election years. As we enter into the third quarter of 2020, rising odds of a feared Democratic sweep might prove to be a stumbling block for the torrid market rally which has so far been driven by unprecedented stimulus from policymakers and optimism over the post-pandemic economic rebound.

We hold an overweight view on in fixed income through Emerging Market High Yield bonds, which provides attractive carry in a search-for-yield environment ahead and relatively firm bottom-up fundamentals in selective areas.

For equities, we see the longer-term risk-reward to be sound as we emerge from the Covid-19 recession and enter the next expansionary cycle, and this underpins our equal weight stance in equities in our asset allocation strategy. Over the near term, however, we see the risks of equity volatility to be higher than average considering that valuations have largely priced in the initial phase of the recovery to 2021, and that major risks related to rising infections, the US elections and US-China geopolitics loom in the backdrop.

Incorporating effective hedges into portfolios would serve to potentially guard against equity volatility. In addition to buying insurance such as using vanilla puts options, an analysis of the largest drawdowns of the S&P 500 since 2009 demonstrate that positions in US Investment Grade Credit and hard currency EM Bonds, as well as positions in gold, JPY versus USD, USD versus EM FX, can act as effective portfolio hedges against equity drawdowns as well (see Exhibit 1).

We do not see this as an opportune time to lean aggressively into an overweight stance in equities, and see this environment as one for selective stock-picking, particularly cyclical and value names that remain undemanding in terms of valuations and would benefit from the global re-opening.

This article was first published by Bank of Singapore on July 3, 2020. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Bank OCBC NISP Private Banking Tbk. or its affiliates.

OCBC NISP Private Banking provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC NISP Private Banking is a part of OCBC Group.